Giỏ hàng

0

TCBH

Hotline

Hotline:

098.588.7187

Thời gian:

Từ 8h - 18h00 Thứ 2 đến thứ 6

Từ 8h - 18h00 Thứ 7 & Chủ nhật

Email:

tanhoangphatdn@gmail.com

Danh mục sản phẩm

Trang chủ

Đóng

Máy đếm tiền

Máy đếm tiền

Đóng

Tất cả Máy đếm tiền

Máy Đếm Tiền AKIO JAPAN

Máy Đếm Tiền XINDA

Máy Đếm Tiền OUDIS

Máy Đếm Tiền HOFA

Máy Đếm Tiền XIUDUN

Máy Đếm Tiền MAXDA

Máy Đếm Tiền MODUL

Máy Đếm Tiền SILICON

Máy Đếm Tiền MANIC

Máy Đếm Tiền GLORY JAPAN

Máy Đếm Tiền MAZSAN

Máy Đếm Tiền Zheyue

Máy Đếm Tiền BALION

Thiết bị siêu thị

Thiết bị siêu thị

Đóng

Tất cả Thiết bị siêu thị

Đầu đọc mã vạch

Đầu đọc mã vạch

Đóng

Tất cả Đầu đọc mã vạch

Đầu Đọc Mã Vạch ZOZO

Đầu đọc mã vạch Honeywell

Máy Pos Bán Hàng, Két Đựng Tiền

Cân Điện Tử

Máy in hóa đơn

Máy in hóa đơn

Đóng

Tất cả Máy in hóa đơn

Máy In Hóa Đơn Xprinter

Máy In Hóa Đơn Antech

Máy In Hóa Đơn Citizen

Máy In Hóa Đơn Epson

Máy in mã vạch

Máy in mã vạch

Đóng

Tất cả Máy in mã vạch

Máy in mã vạch Xprinter

Máy in mã vạch TSC

Máy in mã vạch Godex

Máy in mã vạch Honeywell

Giấy in hóa đơn- Decal tem mã vạch

Giấy in hóa đơn- Decal tem mã vạch

Đóng

Tất cả Giấy in hóa đơn- Decal tem mã vạch

Giấy In Hóa Đơn

Decal Tem In Mã Vạch

Máy chấm công

Két sắt

Két sắt

Đóng

Tất cả Két sắt

Két sắt cơ khí ngân hàng

Két sắt khách sạn

Két sắt thu ngân, công đức

Két sắt điện tử

Két sắt khóa cơ

két sắt vân tay

Máy văn phòng

Máy văn phòng

Đóng

Tất cả Máy văn phòng

Máy hủy tài liệu

Máy hủy tài liệu

Đóng

Tất cả Máy hủy tài liệu

Máy hủy tài liệu Asmix

Máy hủy tài liệu Aurora

Máy hủy tài liệu Balion

Máy hủy tài liệu Bingo

Máy hủy tài liệu Bosser

Máy hủy tài liệu Comet

Máy hủy tài liệu Comix

Máy hủy tài liệu Dahli

Máy hủy tài liệu Silicon

Máy hủy tài liệu DSB

Thiết bị ngân hàng

Thiết bị ngân hàng

Đóng

Tất cả Thiết bị ngân hàng

Máy Bó Tiền

Máy Đóng Chứng Từ

Máy Soi Tiền Giả

Máy Soi Ngoại Tệ

Vật tư kho quỹ ngân hàng

Trình chiếu

Trình chiếu

Đóng

Tất cả Trình chiếu

Máy Chiếu SONY

Đồ dùng gia dụng

Đồ dùng gia dụng

Đóng

Tất cả Đồ dùng gia dụng

Giường Xếp Gọn Đà Nẵng

Máy Lọc Nước RO

Tủ hồ sơ tài liệu,giá kệ

Khuyến mại

Flash Sale

-5%

Két Đựng Tiền Nhỏ 4 Ngăn

Máy Pos Bán Hàng, Két Đựng Tiền

(0)

807,500 đ

850,000 đ

-20%

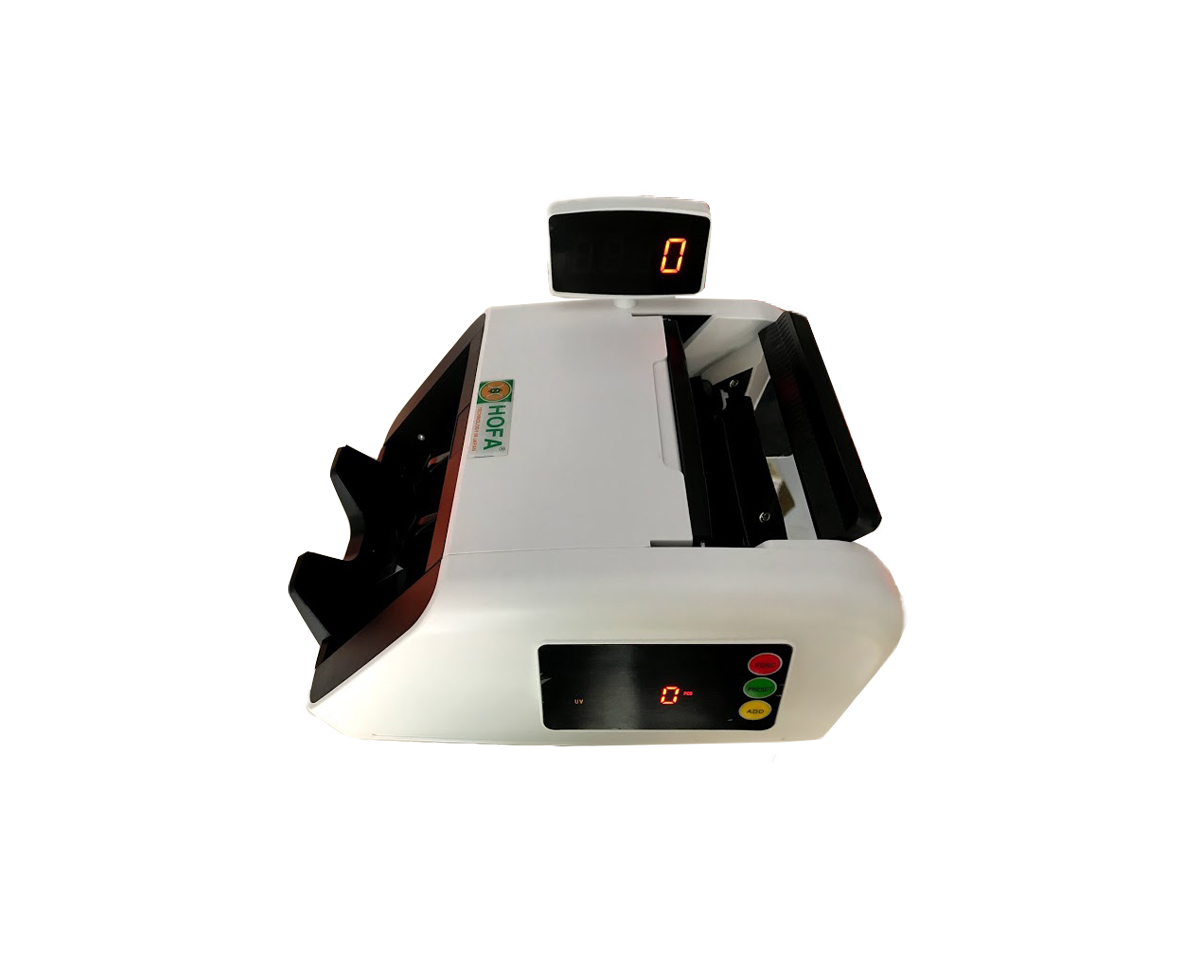

Máy Đếm Tiền HOFA 0306

Máy Đếm Tiền HOFA

(0)

2,800,000 đ

3,500,000 đ

-7%

Máy In Tem Nhãn Mã Vạch Xprinter XP-350B

Máy in mã vạch Xprinter

(0)

1,953,000 đ

2,100,000 đ

-20%

Máy Đếm Tiền Xinda 2165L

Máy Đếm Tiền XINDA

(0)

5,360,000 đ

6,700,000 đ

-15%

Máy Đếm Tiền AKIO JN 2060

Máy Đếm Tiền AKIO JAPAN

(0)

3,145,000 đ

3,700,000 đ

-15%

Máy Đếm Tiền Oudis 5200C [ Máy Đếm Thông Thường]

Máy Đếm Tiền OUDIS

(0)

3,230,000 đ

3,800,000 đ

Máy đếm tiền

Xem tất cả

-7%

Máy Đếm Tiền Akio AD-68

Máy Đếm Tiền AKIO JAPAN

(0)

6,975,000 đ

7,500,000 đ

-15%

Máy Đếm Tiền Xinda Super BC35

Máy Đếm Tiền XINDA

(0)

5,950,000 đ

7,000,000 đ

-15%

Máy Đếm Tiền Xinda Super BC31F

Máy Đếm Tiền XINDA

(0)

6,375,000 đ

7,500,000 đ

-10%

Máy Đếm Tiền Oudis 9799A

Máy Đếm Tiền OUDIS

(0)

8,100,000 đ

9,000,000 đ

-10%

Máy Đếm Tiền HOFA HS88

Máy Đếm Tiền HOFA

(0)

8,730,000 đ

9,700,000 đ

-20%

Máy Đếm Tiền Xinda Super BC31

Máy Đếm Tiền XINDA

(0)

4,320,000 đ

5,400,000 đ

Két sắt

Xem tất cả

-15%

Két Sắt Ngân Hàng BEMC K90SB2

Két sắt cơ khí ngân hàng

(0)

6,375,000 đ

7,500,000 đ

-10%

Két Sắt Ngân Hàng BEMC K250 NHA1

Két sắt cơ khí ngân hàng

(0)

10,350,000 đ

11,500,000 đ

-10%

Két Sắt Hotel Safes WELKO HS42BD

Két sắt khách sạn

(0)

2,790,000 đ

3,100,000 đ

-10%

Két Sắt Hotel Safes HOMESUN HS42E Gold

Két sắt khách sạn

(0)

2,385,000 đ

2,650,000 đ

-10%

Két Sắt Thu Ngân US710 E

Két sắt thu ngân, công đức

(0)

6,480,000 đ

7,200,000 đ

Thiết bị siêu thị

Xem tất cả

-7%

Giấy In Bill K80x45 KHAMI

Giấy In Hóa Đơn

(0)

6,510 đ

7,000 đ

-10%

Máy In Hóa Đơn K58 Xprinter XP-K58

Máy in hóa đơn

(0)

855,000 đ

950,000 đ

-10%

Bộ Rung Tự Phục Vụ 16 Thẻ

Máy chấm công

(0)

4,050,000 đ

4,500,000 đ

-20%

Máy In Hóa Đơn K80 XPRINTER XP-K200L

Máy In Hóa Đơn Xprinter

(0)

1,440,000 đ

1,800,000 đ

-10%

Máy In Hóa Đơn Nhiệt CITIZEN CTS310II

Máy In Hóa Đơn Citizen

(0)

4,410,000 đ

4,900,000 đ

-20%

Máy In Mã Vạch XPRINTER XP-420B

Máy in mã vạch Xprinter

(0)

2,160,000 đ

2,700,000 đ

-10%

Đầu Đọc Mã Vạch ZOZO 2400

Đầu Đọc Mã Vạch ZOZO

(0)

1,530,000 đ

1,700,000 đ

Thiết bị ngân hàng

Xem tất cả

-10%

Máy Bó Tiền MAXDA 8200PRO [ Máy Bó Tự Động Đai Nhựa ]

Máy Bó Tiền

(0)

42,300,000 đ

47,000,000 đ

-10%

Máy Đóng Chứng Từ HJ-50AK [ Máy Đóng Tự Động ]

Máy Đóng Chứng Từ

(0)

24,210,000 đ

26,900,000 đ

-10%

Máy Kiểm Tra Ngoại Tệ HT-106A

Máy Soi Ngoại Tệ

(0)

4,050,000 đ

4,500,000 đ

-20%

Máy Soi Tiền Giả Oudis 09

Máy Soi Tiền Giả

(0)

592,000 đ

740,000 đ

Đồ dùng gia dụng

Xem tất cả

-35%

Ghế Xếp Thành Giường Sumika 168 Tại Đà Nẵng

Giường Xếp Gọn Đà Nẵng

(0)

1,235,000 đ

1,900,000 đ

-15%

Máy Lọc Nước RO FUJIE RO-900CAB Đà Nẵng

Máy Lọc Nước RO

(0)

5,440,000 đ

6,400,000 đ

Hỗ trợ & dịch vụ

Chính sách đổi trả

Kinh nghiệm mua sắm

Hướng dẫn mua hàng

Mẹo vặt cuộc sống

Máy đếm tiền Xinda Super BC31F New 2021 tại TP HCM

Liên hệ mua hàng

Liên hệ hợp tác

Giới thiệu về SALEBUY

Dịch vụ uy tín

Đổi trả trong 7 ngày

Giao hàng toàn quốc

Call Now

Zalo Now

.jpg)

![Máy Bó Tiền MAXDA 8200PRO [ Máy Bó Tự Động Đai Nhựa ]](/public/uploads/files/M%C3%A1y%20B%C3%B3%20Ti%E1%BB%81n%20%C4%90ai%20Nh%E1%BB%B1a%20MAXDA%208200Pro(2).jpg)

![Máy Đóng Chứng Từ HJ-50AK [ Máy Đóng Tự Động ]](/public/uploads/files/M%C3%A1y%20%C4%90%C3%B3ng%20Ch%E1%BB%A9ng%20T%E1%BB%AB%20T%E1%BB%B1%20%C4%90%E1%BB%99ng%20HJ-50AK.jpg)

.jpg)

.jpg)